0 Comments

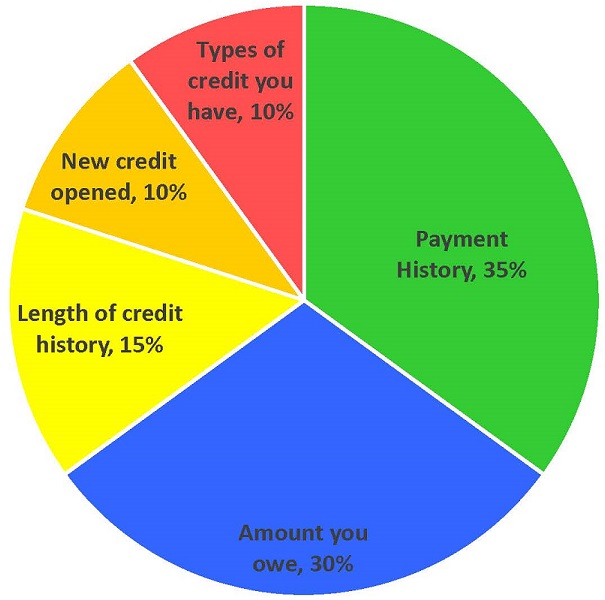

Amount you Owe - 30%

Just because you have it, doesn't mean you should use it. Most credit correction companies will tell you not to use more than 35% of your available credit. That's right, 35%! For example, if you have a credit limit of $1,000 - you shouldn't carry a balance of more than $350 per month. Length of Credit History - 15% When you're cleaning up your credit act, don't close your oldest credit cards. Even if they have a lower credit limit than others, you should still keep them open to maintain that credit history. New Credit Opened - 10% Too many new accounts can negatively impact your score. Not only too many new accounts, but also too many inquiries. NOTE: When purchasing a house and picking a lender, you have a 30 day shopping window to pull your credit several times to do your due diligence and find the best rates and lowest fees. As long as you keep the inquiries all within a 30 day period and you're pulling your credit for the same purpose of getting a mortgage, your credit won't be negatively impacted. Take advantage of this! Types of Credit you Have - 10% You get a bonus for having various types of credit - but don't go overboard. Everything in moderation. If you're a suburbanite with a good job, you likely have/had a car payment, cell phone, a credit card or two and possibly a student loan - that should cover your bases. If you're in the market for your first home, watch this YouTube video to learn all you need to know in just 2 minutes and 39 seconds thanks to the Insurance Information Institute. 1) Find a buyer's agent.

In today's real estate market, there is a lot you can do on your own, but the most important steps require the knowledge and experience of someone who knows the process. There is absolutely no benefit to representing yourself, especially in Virginia, where the seller typically pays buyer agent commission. Do your research and find an agent with a reputable brokerage that you can trust and who has YOUR best interest in mind. 2) Get pre-approved for a mortgage. Before you start touring homes, you want to work with a lender to find out how much house you can afford. Lenders take lots of your financial details into consideration now and things like tax deductions and employment history can impact you in ways you may not have considered. Your buyer agent will likely be able to point you in the direction of a few lenders for you to choose from who they know will get you to settlement. You have 30 days from the day you first pull your credit to pull your credit with several different lenders to shop around for the best rates, so make the most of it! Remember, interest rates also impact your buying power, so take advantage of them while they are low. 3) Establish a budget you're comfortable with. Just because you can get approved for a $500,000 mortgage, doesn't mean you'll necessarily be comfortable with the monthly payments on top of all your other expenses and spending habits. Be sure to establish a budget that you're comfortable with that includes some room for your savings, entertainment expenses, gas and anything else you can't live without spending your money on. 4) Make time! Your buyer agent will guide you through the home buying process, but be sure to make time for it! It is important to attend things like the home inspection, especially for your first home, because there is a lot you will learn about the property and maintenance that could prevent major issues down the line. 5) Listen to your agent. Many times, emotions can take over in the home buying process. There are ups and downs to every transaction, but a good buyer's agent will help give you perspective and advice to guide you through the decision making process during negotiations. It is important to listen to them and try to put emotions aside. |

Fine Nest Realty Group, LLC, A Coldwell Banker Team

2070 Chain Bridge Road, Suite 103, Vienna VA 22182

Kelly Martinez

License ID: 0225209978

571-839-2852 [email protected]

Kelly Martinez

License ID: 0225209978

571-839-2852 [email protected]

Website by Appnector